Car financing is the most popular and seamless way of getting an electric car. According to FCA data, 90% of the vehicles sold in the UK are on finance, and this number is growing year by year. In the UK, the car volume grew by 1% in February 2024 compared with the same month in 2023. The value of the consumer finance business in 2024 is £39 billion in the UK.

Financing an electric vehicle is similar to financing an ICE (internal combustion engine) car, but there are some key differences to consider. Loan terms, the inherent nature of EVs, and available incentives can all impact how financing works for you.

In this article, we will explore how electric car finance works, what are the different types of electric car finance options available, and how other factors, such as insurance and government incentives impact the finance of electric vehicles.

Table of Contents

The Car Finance Overview

Car finance is an umbrella term for borrowing money to buy a car. There are different car finance options, each with its own advantages and considerations.

It's essential to compare different car finance options to find the one that suits you best. These options include personal loans, hire purchase, personal contract purchase (PCP), and leasing. To gain a comprehensive understanding of their differences, check out our guide on car finance and the key differences between PCP and HP.

How Does Electric Car Finance Differ?

Terms

The first key difference is the high cost which affects the car financing terms in various ways. The first is their high prices making the loan amount higher. Unless there is a substantial down payment, the qualifying requirements for the loan can differ compared to getting an average ICE, (internal combustion engine), car.

The lender must see that you have a solid financial profile, and will look for a high credit score and a clean credit history with a stable income to prove that you can afford a high-end vehicle.

There is no specific figure for how much income you need for car finance: The lender evaluates your affordability based on various criteria including debt-to-income ratio, employment status, and living expenses.

Our car finance expert at Motorfinity shares the following tips to improve your chances:

Warranty wise, your average monthly payment for your car should be, at the most, 15% of your monthly income. Based on that statistic, we have calculated some figures for you on the mid-range EVs listed below. The figures are based on a 10% deposit on the car and total finance payments of 60 months, (5 years).

Down Payment (10%) : £4,661.40

Financed Amount : £41,952.60

Monthly Finance : £699.21

Affordable Vehicle Salary: £4666.67

Down Payment (10%) : £4,104.50

Financed Amount : £36,940.50

Monthly Finance : £615.68

Affordable Vehicle Salary: £4104.53

Down Payment (10%) : £3,570.00

Financed Amount : £32,130.00

Monthly Finance : £535.50

Affordable Vehicle Salary: £3570

Down Payment (10%) : £4,521.00

Financed Amount : £40,689.00

Monthly Finance : £678.15

Affordable Vehicle Salary: £4521

The above figures are a guide to help you estimate affordability. In real-world scenarios, costs can vary depending on factors like your credit score, loan terms, down payment, insurance rates, power economy, and maintenance needs.

It's always best to factor in these variables and create a personalised budget before making a final decision.

How Does the Incentives Affect the Electric Car Finance?

The UK Government uses different incentives to encourage the adoption of car finance. It has different incentive programmes for this purpose.

For an overview, see our guide on electric car grants and incentives.

Do the incentives affect car finance?

In an indirect way, a simple answer is yes. Grants and incentives reduce the overall running cost of running an electric car , which lowers the high monthly PCP payment.

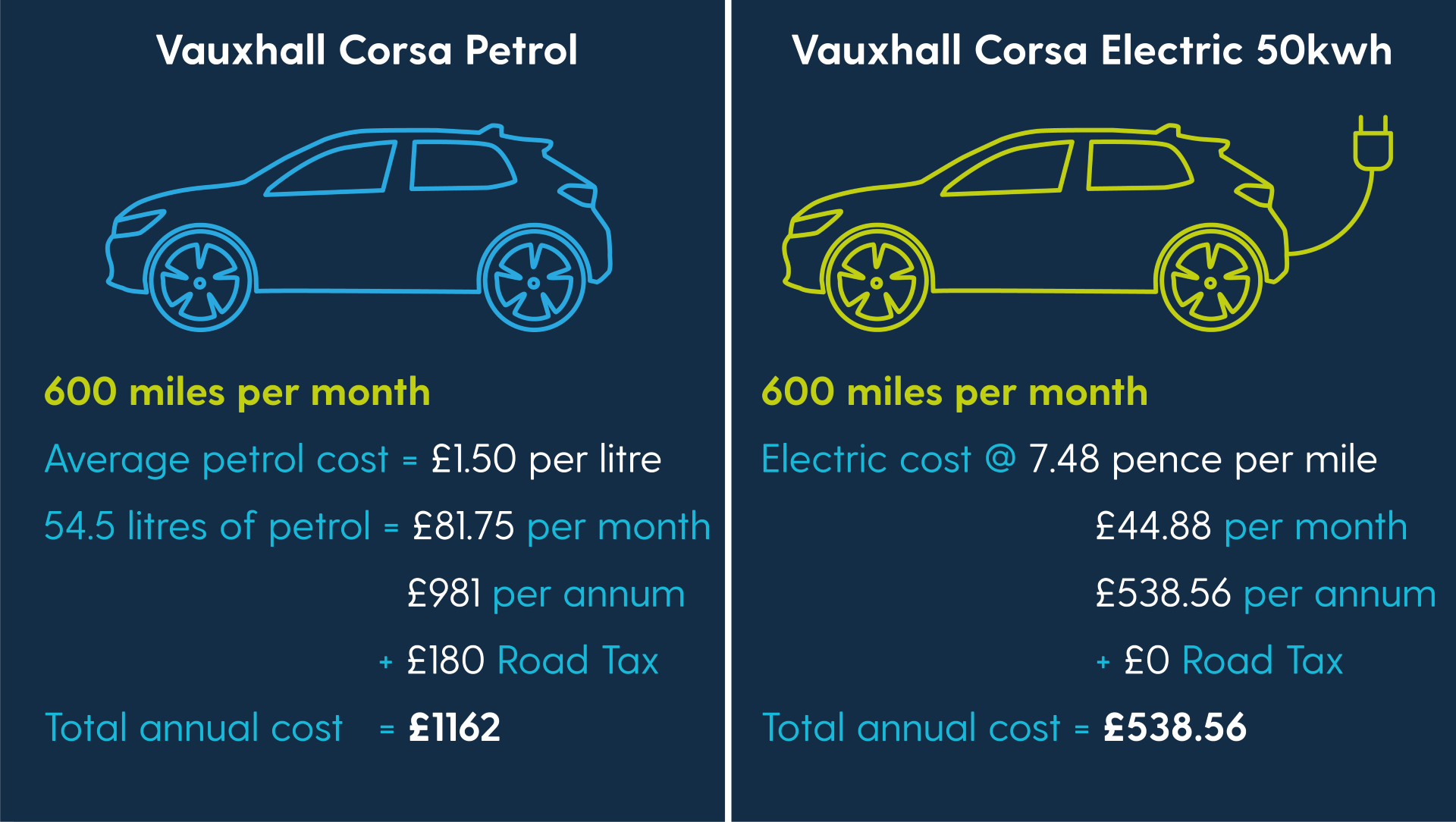

Let's put this into perspective looking at the Vauxhall Corsa Electric and the Vauxhall Corsa petrol variant. We have compiled a cost comparison for you in the infographic below:*

*These figures are an estimation taken from the lease plan EV cost tool. They only consider fuel and road tax and does not include maintenance and other costs.

It is worth noting that electric cars have lower maintenance costs.

Although there is no road tax for the electric variant, it is worth considering that this will change in 2025.

There are also other schemes like Benefit in Kind (BIK) and electric vehicle charge point and infrastructure scheme that can reduce the overall cost of ownership of a Vauxhall Corsa Electric.

How Does Insurance Impact Electric Car Finance?

Insurance does impact electric car finance. Electric cars tends to have a high insurance cost due to their high cost. Also claims involving EVs are generally more costly as compared to the traditional ICE vehicles.

Data plays an important role in the insurance industry. The current data the insurance company has about electric cars is not enough as compared to ICE engines and there is a risk which leads to higher insurance costs. More data does have the potential to reduce the insurance cost in the future.

Factors like the increased availability of parts, more trained mechanics, and lower vehicle values could all contribute to lower costs.

What Types of Electrical Car Finance Are Available?

PCP

PCP, (Personal Contract Purchase), allows you to pay for a car over a period of time. PCP for electrical car finance has pros and cons, depending on your circumstances.

Pros of Getting an Electrical Car on PCP

- Compared to the rest of the finance options, PCP has the lowest monthly payments, which makes it ideal considering the high price tag associated with electric cars.

- GFV, “the future guaranteed value,” becomes more useful for electric cars as it provides a buffer against rapidly changing technology and faster depreciation.

- The main concern about electrical car buyers is the rapidly changing technology of electric cars. This concern can be eliminated if the vehicle is bought through PCP. Offering flexibility at the end of the lease term, it allows consumers to upgrade to newer models with better technology and range.

- PCP is good for overall EV adoption. It has a lower initial cost and flexible terms, making EVs much more accessible. According to the simple law of economics, it can result in more EV demand resulting in greater affordability.

- One condition in the PCP clause is that the vehicle must be kept in good condition and within agreed mileage limits to avoid penalties. This is crucial for maintaining battery life and overall vehicle efficiency.

- PCP is good when it comes to flexibility but what about when you want to keep your electric at the end of the purchase? If you want to keep the car you normally have to pay a final payment which also known as a balloon payment, this can be a big financial burden as compared to other electric car finance options.

- As battery condition plays a vital role in electric car resale value, any degradation beyond normal wear and tear can affect the GFV.

- Considering the uncertainty about electric vehicle technology, factors such as government incentives, new environmental policies, and shift in public preferences affect the GFV.

- Research indicates that PCP makes consumers more vulnerable to economic distress. Factors such as changes in income levels, interest rates, and the residual values of used cars can affect the affordability and feasibility of these agreements. This vulnerability can lead to financial distress or difficulties in managing the balloon payments at the end of the PCP terms.

- The resale market for electric vehicles can be uncertain. As more EVs enter the market, and older models become less desirable. The dynamics of supply and demand can shift. The future trade-in values and overall cost-effectiveness of financing an EV through PCP can be affected.

- A straightforward path to ownership. The hire purchase has no mileage or condition restrictions and allows full ownership after the final payment.

- As discussed, consumers are more prone to economic distress when going for PCP if they want to keep the electric car at the end of the term. HP can relieve that discomfort as it allows users to spread the cost of their EV over a set period without going for any balloon payment, making it easier to manage financially without requiring a significant upfront payment. This makes electric vehicles more accessible to buyers who cannot afford to pay the total price upfront.

- There is no mileage restriction, as in the case of leasing and PCP. This is useful for long-range electric vehicles that users want to use extensively. Electric cars benefit from more extended restrictions; fewer mileage restrictions halt that advantage. If the users do not drive much, they can’t benefit from low cost in the long run.

- Electric vehicles cost more, so the chances of getting car approval are less compared to PCP. Hire purchase has easier approval. Since the car is collateral for the loan, HP agreements might be easier to secure than unsecured loans, especially for buyers with less-than-perfect credit ratings.

- HP agreements typically allow for longer repayment terms compared to PCP agreements. This translates to spreading the cost over a longer period. The maximum term for HP is typically 5 years, while PCP agreements usually max out at 4 years.

- The monthly payments are typically higher as compared to PCP as you are paying towards the full cost of the car.

- With HP, you're generally locked into the agreement until all payments are completed. This lack of flexibility can be a disadvantage. When newer, more technologically advanced or more efficient models become available, you may wish to make a switch.

- The monthly payments are higher than PCP, and the total cost of buying an EV through HP can end up being higher than paying upfront due to interest charges over the agreement term.

- It eliminates the concern of rapid technology advances. PCH is a more appealing option as you can get a car in a relatively shorter period of time.

- No worry about depreciation. Since you don't own the car, you don't have to worry about the depreciation or the hassle of selling the vehicle when you're done with it.

- The opportunity to drive a new car every few years means you can benefit from the latest technology and improved range.

- Many PCH agreements can include maintenance packages, so you don’t have to worry about the cost of servicing and repairs.

- The mileage restriction is an off-putting factor as it does not allow us to get the full benefit of the overall cost of ownership of the electric vehicle.

If your circumstances change and you need to end the lease early, the termination fees can be substantial.

Cons of getting an electric car on PCP

Hire Purchase

Hire Purchase is a finance option where you pay an initial deposit, followed by monthly payments until the vehicle's total value is paid off. At this point ownership transfers to you.

Pros of getting an electric car on HP

Cons of getting an electrical car through HP

Leasing an Electrical Car

PCH is another option to finance your leasing car. It is a popular method for individuals who want to lease a vehicle without the intention of buying it at the end of the lease term. Consider it a long-term rental of an EV.

Pros of getting an electrical car through PCH

Cons of getting an electric car through PCH

What is a Battery Car Lease?

A battery car lease involves leasing the car battery while purchasing the remainder of the vehicle. This arrangement is beneficial as it lowers the upfront cost of the car, since the battery — one of the most expensive components of an electric vehicle — is not included in the purchase price.

It provides a warranty for the battery's condition. If the battery fails or degrades significantly, the manufacturer will replace it. Typically, the monthly lease cost ranges from £50 to £100.

Motorfinity

At Motorfinity, we pride ourselves on offering exclusive discount across all makes and models. Whether you're looking for efficiency, style, or cutting-edge technology, our selection is designed to meet every need.

You can choose from Personal Contract Purchase (PCP), Hire Purchase (HP), and leasing deals. Each option provides flexibility and benefits tailored to different driving habits and budgetary needs.

Are you eligible?

Our nation’s Armed Forces, Veterans, Emergency Services, NHS, Police and Prison Services, the Education and Social Care sectors and more form our eligible audience.

Related Car Reviews and Articles

Understanding Electric Cars: Grants, Incentives and Tax Credits

Estimated Read Time: 3 minutes

Considering a switch to an electric vehicle (EV) but worried about costs? You're not alone. Thankfully, various governments and organisations offer grants, incentives, and tax credits to make eco-friendly travel more affordable.

Read More

PCP vs HP?

Estimated Read Time: 2 minutes 30 secIf you’re looking to buy a car on finance, two of the most popular options that you will be presented with are Personal Contract Purchase (PCP) and Hire Purchase (HP) Finance. In this article we explore key differences between PCP and HP finance, as well as the pros and cons of each to help you decide which one is right for you.

Read More

The Difference between Plug-in, Mild, and Hybrid Vehicle Technologies: A Detailed Guide

Estimated Read Time: 3 minutes 30 sec

If you've recently started learning about hybrid cars, but are confused by the many types, you're not alone. In this easy-to-understand guide, we will carefully go through the differences. We will look at why hybrids exist, what makes each one different, and what special features make each one stand out. Table of Contents

Read More